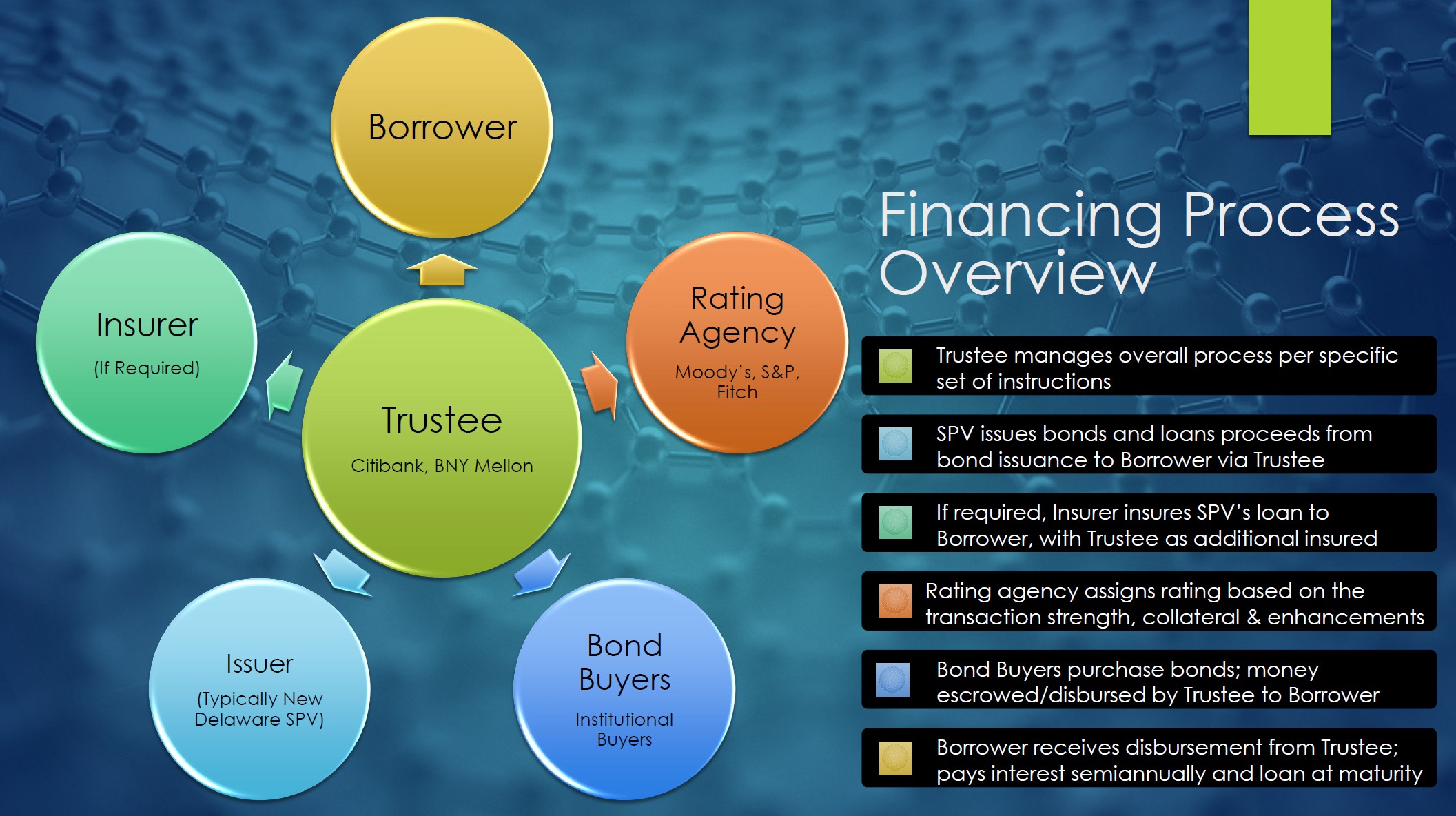

We provide financing for large-scale projects requiring a minimum of $10 million and up. Our Project Financing Program provides up to 100% debt financing for energy projects, commercial real estate and infrastructure projects, government projects and growth-stage companies. Bonds are issued from a newly-created Special Purpose Vehicle (SPV) backed by client-provided collateral, i.e., government guarantees, bank guarantees, or other assets such as signed offtake agreements, marketable securities, precious metals, etc.

Program Requirements

We will consider commercially viable projects in virtually any geographic area throughout the world including North and South America, the Caribbean, Western/Eastern Europe, Australia/New Zealand, Southeast Asian (ASEAN) countries, China, India, Africa and the Middle East. Our typical loan size is $10 million and up, interest only, with a repayment period of 3-5 years. In most cases, some portion of the interest will be prepaid from the loan, allowing the borrower to focus on repayment of principal at maturity.

Qualified Assets as Collateral

The key to our program is the client’s ability to provide a qualified asset as collateral, other than direct project assets such as real estate, land or equipment. Qualified assets include almost any type of liquid or near-liquid asset including standby letters of credit, bank guarantees, offtake agreements, publicly-traded stock, precious metals/precious gems, etc. (see below for a list of Qualified Assets). Once the Qualified Asset has been accepted by our Trustee, i.e., Citibank, N.A., the time to funding is approximately 90 – 120 days.

Program Benefits

- 100% project financing potential for borrower;

- Allows borrower to raise patient capital without sacrificing equity;

- The loan proceeds can be used as debt or equity capital, investor buy-outs, down payments, re-financings, etc.;

- Ability to obtain financing quickly—usually in 90 – 120 days, or less;

- No restrictions on use of capital as long as used for prescribed purposes.

List of Qualified Assets

- Standby letters of credit, bank guarantees;

- Sovereign & sub-sovereign guarantees;

- Offtake agreements, i.e., signed purchase power agreements (PPAs);

- Marketable securities, i.e., stocks, bonds, preferred shares of stock, index funds, or ETFs;

- U.S. Treasury bills (T-bills), bonds, mutual funds, and money market funds;

- Retirement investment accounts: 401(k)s, IRAs, etc.;

- Pensions, annuities, royalties;

- Certificates of Deposit (CDs), promissory notes;

- Gold, precious metals, precious gems, jewelry, artwork, collectibles;

- Hard/soft commodities, i.e., oil, natural gas, minerals, corn, wheat, etc.;

- Business inventory.

Our Process

"*" indicates required fields